- 16/02/2018

- Posted by: Nick Lucey

- Category: Finance & accounting, Financial Planning, Funding trends, Investments, Mortgage Broking

What is goals-based lending advice and why is it effective?

Summary / key points

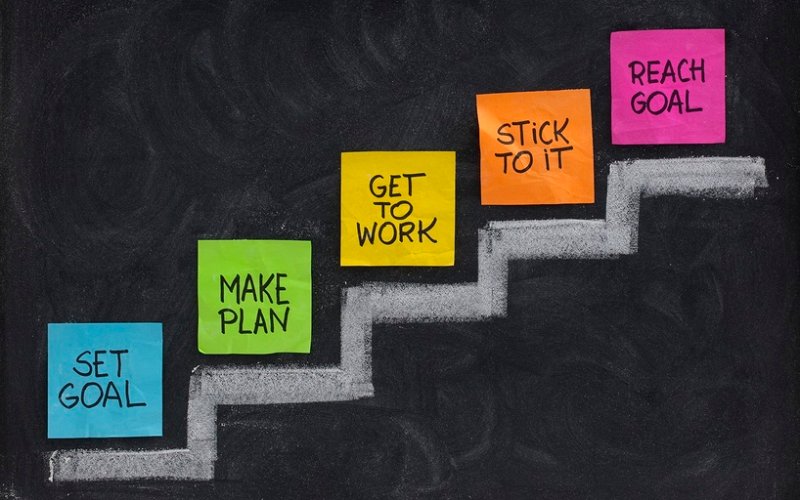

- Goals based lending focuses on your goals and dreams first, then the loan and product at the end as a tool to get there.

- It’s about creating a financial plan and reviewing it to help you achieve goals

- It provides a supportive and encouraging role as a mortgage broker, rather than tick and flick

When I’ve spoken to other people who have sought advice for a loan or even when I spoke to the bank about my first loan, it seemed like the focus was purely on interest rate or product. The bank lender or mortgage broker usually says something like “I can save you 0.8% on your loan if you refinance with this product now”. There is nothing wrong with that, why wouldn’t anyone want to save money? But the fact is, interest rates change all the time and while you save 0.8% this year and 0.3% the following, it might become 1% more expense in the 3rd year. You’re plan could be to shop around and refinance your loan every 2 years, pay the discharge fees and get the best deal for you. Or, we’ve adopted an approach called goals-based lending, which we believe adds purpose, value and real plan to help you achieve what’s most important to you.

Goals based lending takes the time to look at the bigger picture, discover why this loan is important to you and what’s driving the motivation to borrow all this money. Everyone has a dream or goal that is important to them, but dreams and goals don’t often become reality, unless you have a plan to achieve them. You’ll also need someone to keep you accountable and stay on track along the way.

We’ve turned the old, outdated model of focussing on interest rates and products around to focus on creating a real financial plan that is designed to turn your dreams and goals into reality. The loan is just a product that will help us get there. It is the last thing we look at after we have identified your goals, reasons behind it and worked out a budget, repayment strategy and timeframe.

I went to a personal trainer a while ago and the first thing they asked me was, “what is your goal”? I said; “I want to build muscle and lose fat”. They said, “that’s great, I can help you with that, but why do you want to do that”? I was a little surprised by his response as I thought that was obvious! But I replied, “because I want to look good naked” (quote from Lester Burnham). As vain as this was, it wasn’t until that point when I had articulated a reason to get up early, get myself to the gym and the motivation to achieve my goal, that I had something spurring me on. The personal trainer helped me to understand that if I had a fitness goal, then I needed a reason why it was important and a reason to achieve it and that would be what would keep me on track and ensure I achieved my end goal.

The other important thing that helped me achieve my fitness goal was having a coach to provide advice and support, encourage me and make me feel good about my progress. The most elite athletes in the world and most successful business people have coaches and mentors. It’s not because they don’t know what to do, but a coach provides the support and positive feedback people need to reach their dreams and goals. A Coach helps to monitor and review progress so that the bigger goal can be achieved each step at a time. There is a great TED talk on having a coach here. So why doesn’t this happen in the lending game?

At Nest Advisory, we have adopted this coaching approach to the way that we provide lending advice to our customers as part of our overall goals based lending. We believe it is important to help customers realise their big picture goal, reason why they want to achieve it, then set up a plan and coach them along the way with reviews to help dreams become realities.

For example

Ruth comes to see me for help with her home loan. Initially Ruth tells me she would like to save money on her loan. I then discover that the reason Ruth wants to save money on her loan is because she would like to take her family on an overseas holiday but struggles to save the money to do it. I asked her where she wants to go and why this is important to her. Ruth tells me that growing up, her family didn’t have the money to go on overseas trips and she wanted her children to have that experience that she never got.

Now that we have a goal and a reason why it is important, we start to create Ruth’s financial plan so that she can take her family on a holiday. This involves going through her income and expenses, choosing a time when to go on holiday, how much it will cost and what she will need to do to achieve this.

We work out that Ruth needs $10,000 in 2 years or $5,000 a year, or $416 per month or $96 a week. After going through some expenses, we created a budget that would save her $70 a week, which would be saved in a new offset account. We then switch her loan to save her another $53 a week, which would also be saved in her offset account. With the new budget, Ruth doesn’t have to worry about bills coming in, buying lunches at work or buying that H&M shirt on sale because all these things have been accounted for while she maintains her savings plan. We review the plan on a regular basis. Ruth feels good about being in control and on her way to achieving her goal through our plan, encouragement and support. She feels motivated to achieve this goal because we have defined her reason for doing this.

With the goals based lending strategy, Ruth has been able to save her money and achieve her ultimate goal of taking her family on an overseas holiday.

Get in touch

If you would like to review your lending goals and create a plan to achieve them, don’t hesitate to get in touch here

Regards,

Nick